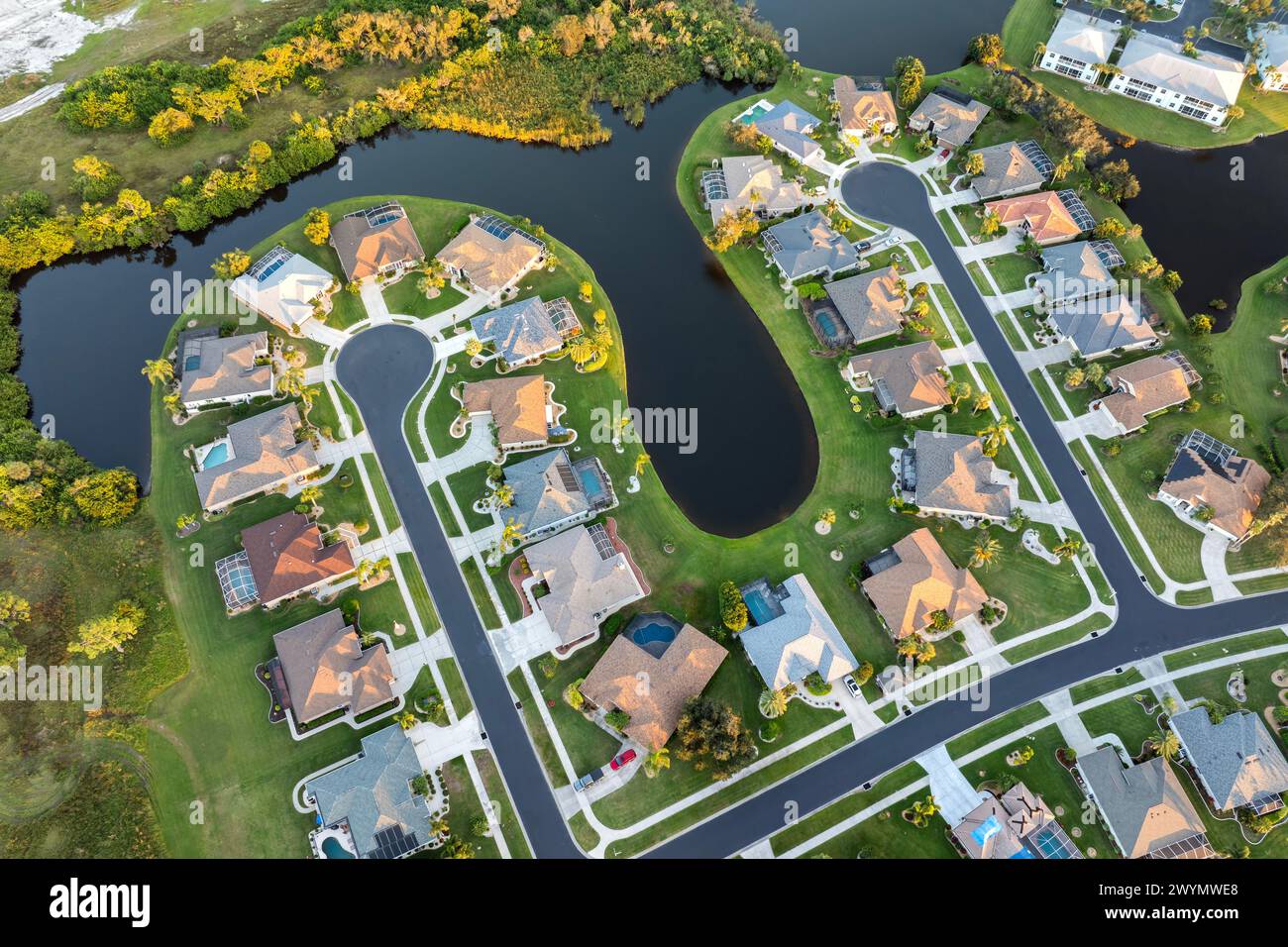

Four decades of pricing data just delivered a verdict on the American housing market, and it isn’t a comforting one for anyone hunting for a starter home. A new analysis of the Freddie Mac House Price Index, spanning 385 metro areas since 1986, has identified 25 markets where home values didn’t just climb, they went parabolic. That word choice matters. Parabolic price action is a term borrowed straight from trading desks, and when it shows up in residential real estate, it signals a structural imbalance that outlasts any single rate cycle.

A Housing Story That Refuses to Normalize

The Federal Reserve has spent three years trying to cool a housing market that barely blinked. Mortgage rates spiked, affordability metrics deteriorated, and still, in dozens of metros, prices kept grinding higher. What the Fast Company analysis makes clear is that this isn’t a 2020-2022 pandemic anomaly. It’s a four-decade trend, and the metros at the top of that list have effectively decoupled from wage growth and local income fundamentals.

This divergence is playing out unevenly across the country. As we detailed in our recent coverage of the luxury housing surge against a stalling mainstream market, the split isn’t just geographic, it’s also a function of price tier. High-end coastal and Sun Belt properties keep finding buyers with cash or substantial equity, while entry-level inventory remains scarce and expensive relative to local incomes.

Key Data Points Investors Should Track

- The Freddie Mac House Price Index covers 385 metro areas, and 25 of them rank as the most extreme price appreciation cases since 1986, according to Fast Company’s analysis.

- Regional development activity continues despite affordability concerns: Charlottesville, Virginia is set to add a 1,332-bed apartment complex, VERVE, by summer 2027, replacing nine existing residential buildings adjacent to the University of Virginia.

- Vermont’s Chittenden County continues to face delayed housing and infrastructure projects, according to local reporting, reflecting a broader supply bottleneck common across mid-size U.S. metros.

- Internationally, Egypt has moved to end a 1996-era cap on foreign real estate ownership, a policy shift explicitly designed to attract foreign capital into its property sector.

- Tokyo’s property boom is drawing scrutiny from regional macroeconomic monitors, with the ASEAN+3 Macroeconomic Research Office framing rising prices amid demographic decline as a stability warning rather than an immediate crisis.

What This Means for Rates, Buyers, and Portfolio Positioning

The persistence of parabolic price gains in specific U.S. metros complicates the Fed’s inflation calculus. Shelter costs remain one of the stickiest components of core CPI, and a housing market that refuses to soften in its most expensive corners undercuts the disinflation narrative markets have been pricing in. For homebuilders and REITs exposed to those 25 overheated metros, the setup is double-edged: pricing power remains intact, but affordability ceilings are getting closer to a breaking point that could trigger sharper corrections than a gradual cooling.

Globally, the Egyptian and Japanese cases underline a parallel dynamic. Capital is chasing real assets wherever restrictions loosen or demographic scarcity persists, and that flow doesn’t discriminate by border. Investors with exposure to real estate investment trusts, homebuilder equities, or mortgage-backed securities should treat regional divergence, not national averages, as the operative signal going forward.

Watch the next Freddie Mac index update and any Fed commentary on shelter inflation closely. If parabolic metros keep outrunning wage data, expect renewed political pressure on affordability policy heading into the back half of 2026.