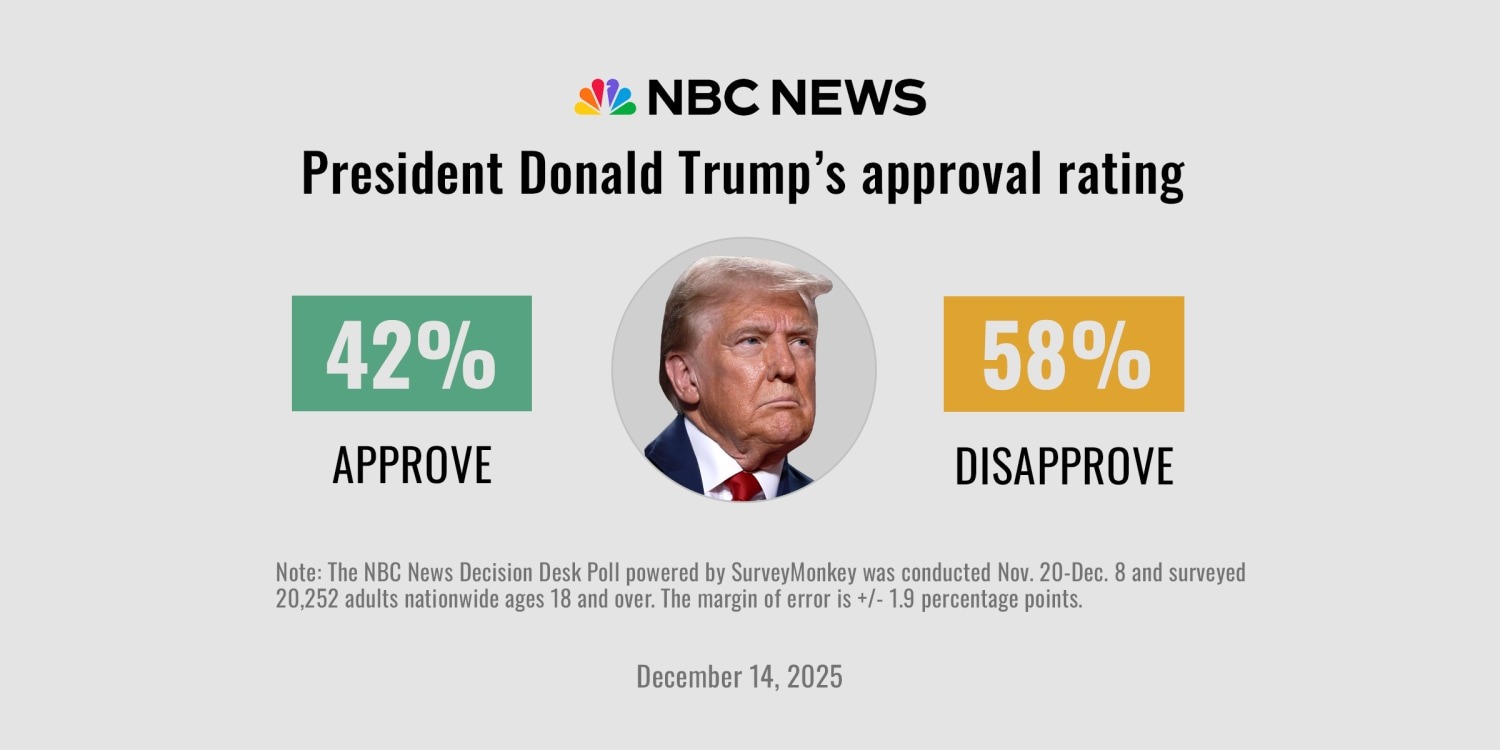

At just 30% approval in the latest American Research Group poll, President Donald Trump has hit the weakest standing of his second term, a number that carries direct implications for fiscal policy, market sentiment, and the congressional balance of power heading into the 2026 midterms.

A Political Signal With Real Economic Consequences

Presidential approval ratings are not merely political scorecards. For financial markets, they function as a leading indicator of policy continuity risk. A president operating below 35% approval faces mounting legislative resistance, reduced capacity to push through budget priorities, and heightened probability of a midterm reversal that could reshape the fiscal landscape entirely.

The timing here is striking. The American Research Group poll, cited by USA Today and Newsweek, places Trump at 30% approval as of late June 2026. Separate MSN-aggregated data shows a broader national average hovering between 37% and 38%, with net approval declining across all 50 states since January 2025. That is not a regional story. That is a structural erosion.

Internationally, the damage is equally pronounced. A 36-country Pew Research Center survey published June 23 finds declining confidence in the United States as a reliable partner, with rising concerns about U.S. foreign policy direction and democratic governance. For multinational corporations and foreign investors holding dollar-denominated assets, that perception shift matters.

The Midterm Arithmetic and Its Market Implications

Time Magazine’s analysis of Pennsylvania as the pivotal battleground for House control underscores what markets are beginning to price in: a credible scenario in which Democrats recapture the House in November 2026. Historically, divided government has produced mixed but often market-friendly outcomes through fiscal gridlock, but the current context is different.

The Trump administration’s legislative agenda, including tax provisions, tariff structures, and deregulatory priorities, depends on Republican congressional majorities. A House flip would effectively freeze that agenda. Bond markets would likely reprice fiscal risk downward as deficit-expanding legislation stalls, while equity sectors that have benefited from deregulation, including energy, financials, and defense, could face renewed headwinds.

As we outlined in our recent analysis of geopolitical risks rattling U.S. equity futures, the combination of foreign policy uncertainty and domestic political fragility creates a compounding risk environment for investors through the second half of 2026.

What the Data Is Actually Telling Investors

Several data points from the past 48 hours deserve close attention:

- 30% approval in the American Research Group poll, the lowest recorded figure of Trump’s second term, per USA Today.

- 37-38% national average across aggregated polling, with net approval negative in all 50 states since January 2025, per MSN-compiled data.

- 36-country Pew survey showing declining international confidence in U.S. reliability as a global partner, published June 23, 2026.

- Pennsylvania identified as the decisive swing-state battleground for House control in 2026 midterms, per Time Magazine analysis.

The underlying risk here is not simply electoral. It is the policy uncertainty premium that markets must now absorb. When a president’s approval falls this sharply, the probability distribution of legislative outcomes widens considerably. Investors pricing in a clean extension of existing tax and trade policy face a materially higher risk of disruption than consensus estimates may reflect.

The Federal Reserve’s own trajectory adds another layer of complexity. As detailed in our coverage of the Fed’s hawkish shift under Chair Warsh, monetary policy is already tightening into a politically fragile environment, a combination that historically amplifies volatility around midterm cycles.

Watching the Weeks Ahead

The next 90 days will be critical. Congressional budget negotiations, any movement on tax legislation, and further polling releases will calibrate how aggressively markets adjust their political risk premium. Watch for shifts in Treasury yields as fiscal expectations evolve, sector rotation away from deregulation beneficiaries, and the dollar’s behavior against major currencies as international confidence data continues to accumulate. The 30% approval print is a threshold that, historically, has preceded significant legislative paralysis. Markets should treat it accordingly.

Frequently Asked Questions about Trump Approval Rating and Market Impact

Why does a presidential approval rating matter to financial markets?

Presidential approval ratings directly affect a president’s ability to pass legislation, maintain coalition support in Congress, and execute policy priorities. When approval falls sharply, the probability of key fiscal, trade, or regulatory legislation advancing drops, creating policy uncertainty that markets must price in. Investors in sectors sensitive to government policy, including energy, financials, and healthcare, pay close attention to these trends.

What does a 30% approval rating mean historically for a sitting president?

A 30% approval rating places a president among the weakest performers in modern polling history. Gallup data tracking presidents from Harry Truman onward shows that approval at this level typically signals severe legislative headwinds and a high probability of significant midterm losses. It does not guarantee a specific electoral outcome, but it materially increases the risk of divided government.

How could a Democratic House majority after the 2026 midterms affect investors?

A House flip would likely stall or reverse key elements of the Trump administration’s fiscal agenda, including potential tax extensions and deregulatory measures. Sectors that have benefited from lighter regulatory oversight, such as energy, banking, and defense, could face renewed pressure. Conversely, fiscal gridlock might reduce deficit expansion fears, providing some support to long-dated Treasury bonds.

What does the Pew Research international survey signal for the U.S. dollar and foreign investment?

The 36-country Pew Research survey showing declining confidence in U.S. reliability as a global partner introduces a soft but meaningful risk for dollar-denominated assets. When international confidence in U.S. governance erodes, foreign capital flows can slow or redirect toward alternative safe-haven assets. Over the medium term, sustained reputational decline can weigh on the dollar’s reserve currency premium, though this is a gradual process rather than an immediate market shock.

Which key indicators should investors monitor over the next 90 days?

Investors should track further polling releases for trend confirmation, congressional vote counts on budget and tax legislation, Treasury yield movements as fiscal expectations shift, and sector performance in deregulation-sensitive industries. Any acceleration in the approval decline toward the mid-20s would represent a significant escalation of political risk. Pennsylvania polling and House generic ballot surveys will serve as the most direct electoral barometers.

Stay ahead of the markets. Every day, LeGrebe delivers expert financial analysis on the trends and decisions shaping the North American and global economy, in under 5 minutes.